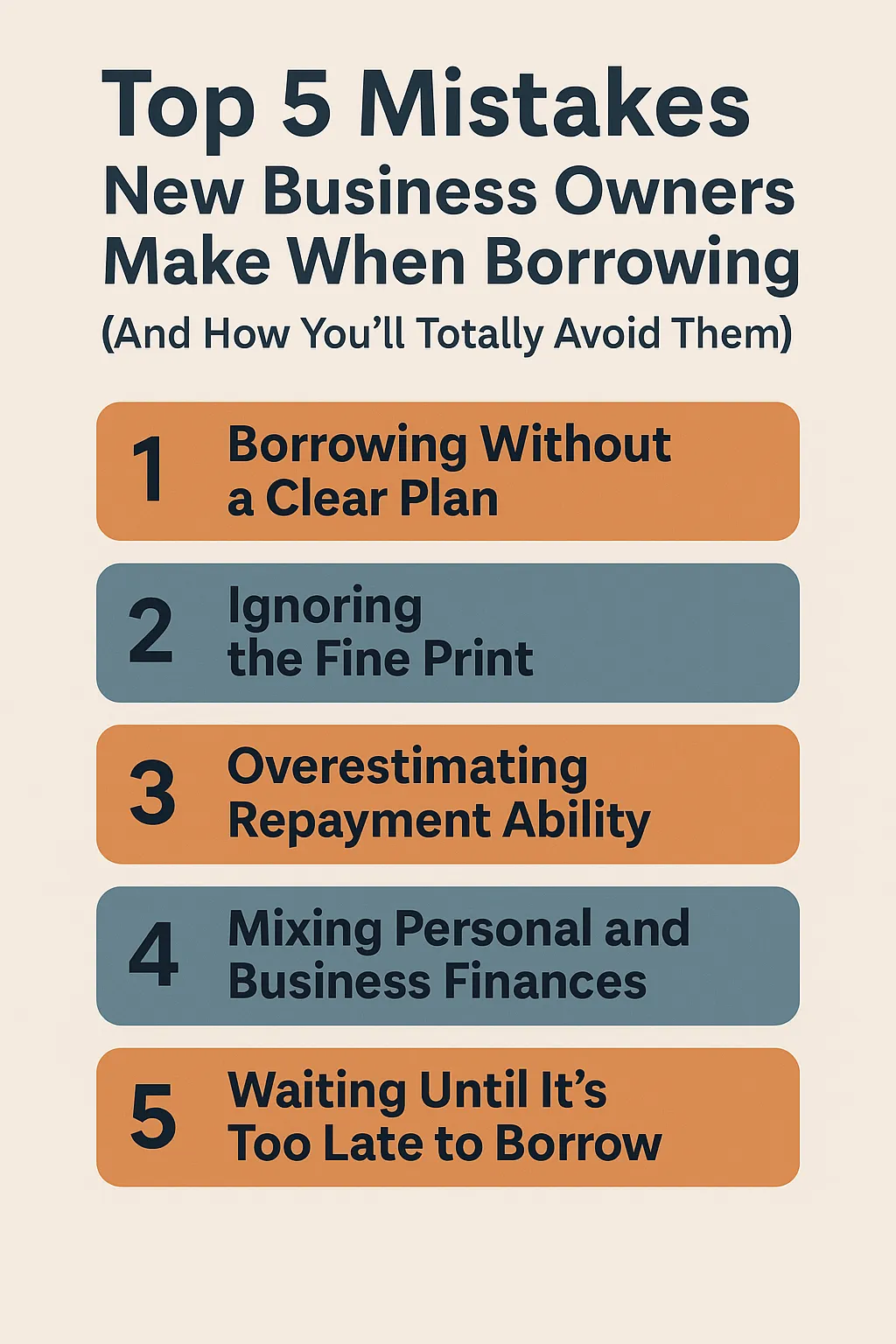

Top 5 Mistakes New Business Owners Make When Borrowing (And How You’ll Totally Avoid Them)

Starting a business is exciting—ideas flowing, dreams unfolding, and opportunities opening up. But when it comes to borrowing money, many new entrepreneurs hit speed bumps they didn’t see coming. Borrowing can be a smart move to fuel growth, but only if you avoid the common traps that leave business owners stressed (and lenders unimpressed).

Here are the top five mistakes new business owners make when borrowing—and how you can totally avoid them.

1. Borrowing Without a Clear Plan

The Mistake: Jumping into a loan just because funds are available.

Many new owners think, “If I get approved, I’ll figure out how to use the money later.” But lenders want to see a clear purpose, and you want to make sure that borrowed money will actually grow your business—not just cover random expenses.

How to Avoid It: Before applying, map out exactly how much you need, what it will be used for, and how it will create a return. A loan should be an investment, not a safety net.

2. Ignoring the Fine Print

The Mistake: Skimming over loan terms because the approval feels like a win.

From hidden fees to prepayment penalties, overlooking the fine print can lead to major surprises.

How to Avoid It: Read every line of your agreement and don’t be afraid to ask questions. If something feels unclear, ask your lender to explain in plain language. Transparency is your right.

3. Overestimating Repayment Ability

The Mistake: Assuming sales will skyrocket and cash flow will always be steady.

Too many new entrepreneurs borrow based on their best-case scenario, not reality.

How to Avoid It: Build a repayment plan based on conservative projections. Ask yourself: If my revenue dips for a few months, can I still handle this loan? If the answer is no, adjust the amount you borrow or look for more flexible terms.

4. Mixing Personal and Business Finances

The Mistake: Using personal credit cards or loans for business expenses—or worse, blending them together.

This makes tracking business performance a nightmare and can put your personal financial health at risk.

How to Avoid It: Keep your business finances separate from day one. Open a business bank account, establish business credit, and apply for loans under your business name. This not only protects you personally but also builds credibility for future funding.

5. Waiting Until It’s Too Late to Borrow

The Mistake: Only seeking a loan when you’re already desperate.

Lenders are more hesitant to approve applications when your cash flow is weak or your credit has taken a hit.

How to Avoid It: Be proactive. Apply for financing while your financials are strong and your business is stable. Think ahead to what your business will need 6–12 months from now, not just today.

Final Thoughts

Borrowing can either be a stepping stone or a stumbling block for your business. The difference lies in preparation, awareness, and discipline. By avoiding these five common mistakes—borrowing without a plan, ignoring fine print, overestimating repayment, mixing finances, and waiting too long—you’ll set yourself up to use business loans as a growth tool, not a burden.

The bottom line? Smart borrowing fuels success. Rushed borrowing fuels regret